The UK 24-Month Rule: When Employees on Short UK Assignments Can Claim Rent, Travel and Other Costs

When an employee is sent to the UK for a limited period, one of the first questions is usually this: can they claim tax relief for their rent, travel and living costs while they are here?”

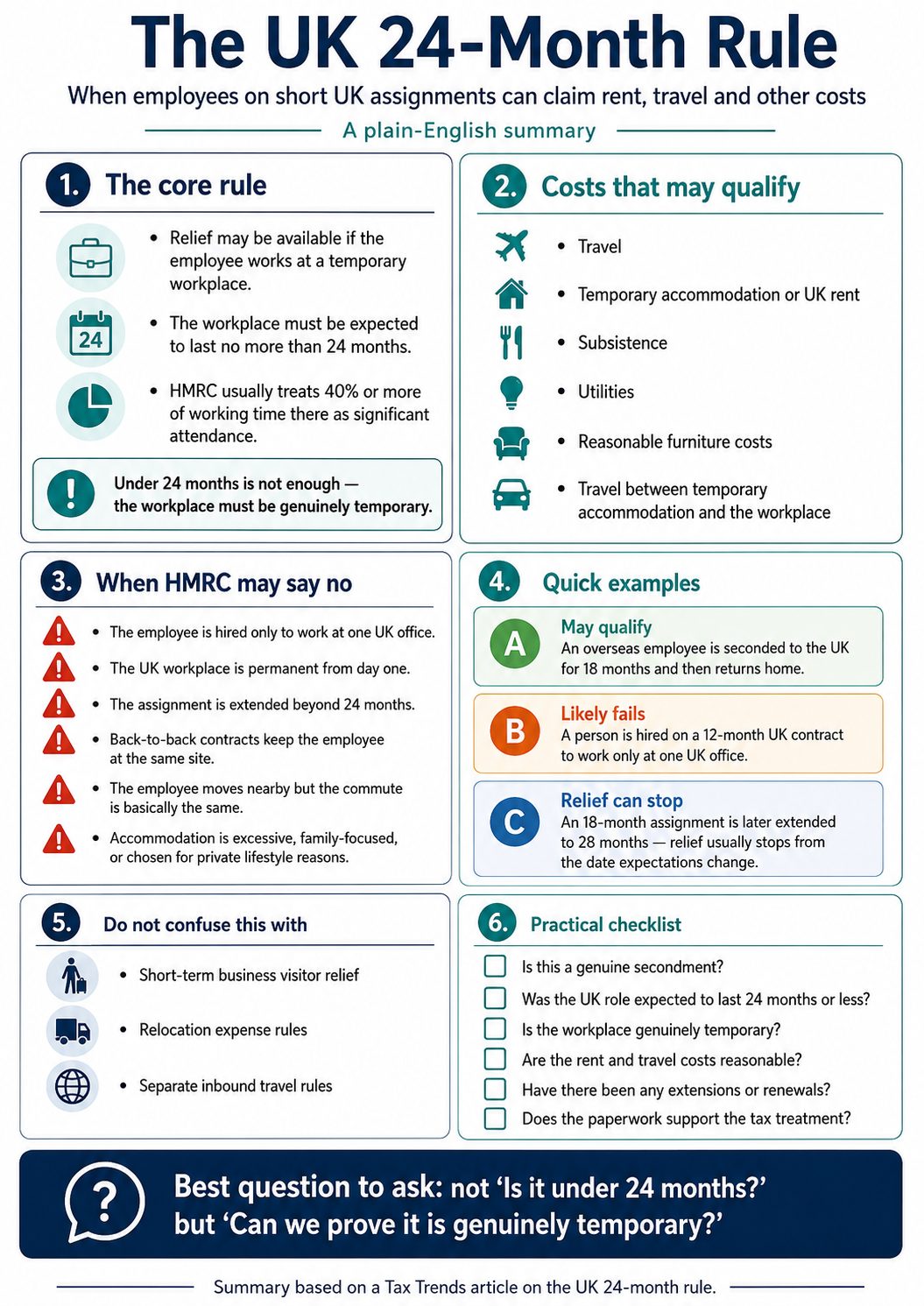

But this is where many people get caught out. The UK “24-month rule” is not a magic rule that says every assignment under two years is tax-free or deductible. It is more subtle than that. A 12-month or 18-month UK contract can still fail. Equally, a longer international arrangement may qualify for relief at the beginning and then stop qualifying later.

The key issue is whether the employee is working at a temporary workplace, not simply whether the contract says “less than 24 months”. That distinction matters because, where the UK workplace is genuinely temporary, the employee may be able to claim relief for:

- Travel

- Accommodation

- Subsistence

- Utilities

- Some related costs

Where the UK workplace is treated as permanent, those same costs may simply be ordinary commuting and private living expenses. That is the difference between a legitimate tax-efficient secondment and a nasty PAYE/NIC problem waiting to happen.

The Basic Idea

The UK tax rules allow relief for travel to a temporary workplace. A temporary workplace is somewhere the employee attends for a limited job, project, assignment or other temporary purpose.

If the employee is simply working at their normal place of work, the costs of getting there and living nearby are normally private costs.

The 24-month rule then adds a further test. Broadly, if the employee is expected to work at that workplace for more than 24 months, and spends a significant amount of their working time there, the workplace is treated as permanent.

HMRC usually treats “significant” as 40% or more of working time.

So the practical test is not just: “Is the contract less than 24 months?” but “Is this genuinely a temporary workplace, and was the employee expected to be there for no more than 24 months?” That is a much more dangerous question.

The Trap: A Short Contract Does Not Always Mean a Temporary Workplace

This is the point most people miss. If someone is hired on a 12-month UK contract to work at one UK office, and that office is the whole purpose of the employment, HMRC may say that the office is a permanent workplace from day one.

Why? Because the employee has not been temporarily sent somewhere as part of a wider continuing employment. The UK office is simply where the job is. This is especially important for inbound employees. There is a big difference between:

- An overseas employee sent to the UK for 18 months, who will return to their overseas employment afterwards; and

- Someone employed on a 12-month UK contract where all the duties are carried out at one UK location.

The first may qualify. The second may not. The label in the contract helps, but it is not decisive. Calling something a “secondment” does not make it one. HMRC and the tribunals will look at what is really happening.

What Costs Can Qualify?

Where the UK workplace genuinely qualifies as temporary, the relief can be wider than many people expect. It is not just flights and train fares.

Depending on the facts, relief may be available for:

- Travel to and from the temporary workplace

- Temporary accommodation

- Rent on a UK flat

- Hotel costs

- Subsistence, such as meals while travelling

- Utilities connected with temporary accommodation

- Reasonable furniture costs for the temporary accommodation

- Travel between the temporary accommodation and the temporary workplace

HMRC’s own guidance includes an example where the rent of a UK flat can qualify during a 15-month UK secondment, even where the employee sold their home-country flat and did not keep accommodation overseas. That is helpful. But it is not a blank cheque. The cost must still be:

- Reasonable

- Additional

- Linked to the business travel

If the employee chooses a more expensive location for personal reasons, or rents a large family property when only modest employee accommodation is needed for the assignment, relief may be restricted. HMRC’s view is basically this: Reasonable temporary accommodation for the employee may qualify. Lifestyle choices do not.

Rent: The Most Misunderstood Cost

Rent is the cost most likely to cause confusion. People often assume rent is always private. That is not quite right. If the employee is genuinely on a temporary UK secondment, UK rent may be deductible or reimbursed tax-free, provided the workplace is temporary and the rent is an additional cost of working in the UK.

But if the UK workplace is permanent, the rent is usually just the cost of living near work. That is private. This is where the facts matter. A modest flat near the UK workplace for an 18-month secondment may be fine. A large family house because the spouse and children are relocating may need to be split, with relief limited to the reasonable employee-only business cost. A luxury property in a preferred location, miles from the workplace, chosen for private reasons, is asking for trouble. The sensible approach is to separate the rent into categories:

- Reasonable business accommodation

- Extra cost for family members

- Extra cost caused by private location choice

- Utilities

- Furniture

- Weekend or private use

- Travel from the accommodation to the workplace

Do this at the start. Trying to reconstruct it after HMRC opens an enquiry is not a sport anyone should take up voluntarily.

What Happens If the Assignment Is Extended?

This is another common trap. Suppose the employee is sent to the UK for 18 months. At the start, everyone genuinely expects the assignment to end after 18 months. The workplace is temporary and relief is claimed. Then, after 10 months, the assignment is extended so the total expected period becomes 28 months.

In that case, the relief does not necessarily fail from day one. It usually stops from the date the expectation changes. So the first 10 months may be fine. From the date the extension is agreed, the workplace may become permanent. The payroll treatment should change immediately. This is where many employers get caught. They carry on reimbursing rent and travel tax-free after the point when the facts have changed. The rule is prospective, but it is not optional.

What If There Are Two Contracts?

A second contract does not automatically restart the clock. If an employee has an 18-month contract at the same UK site, followed by another contract at the same site, HMRC may treat the work as one continuous period. The result may be:

- Relief for the first 18 months, if the original expectation was genuinely under 24 months

- No relief once the second contract means the employee is expected to spend more than 24 months at the same workplace

The same issue can arise with rolling extensions. A project that is “temporary” every six months can still become permanent for tax purposes once the expected total period goes beyond 24 months. HMRC has seen this film before.

What If the Employee Moves to Another Nearby Site?

Moving workplace does not always restart the 24-month clock either. If the employee moves from one office to another nearby office, and the commute is broadly the same, the locations may be treated as one workplace. For example, moving from one building in the City of London to another nearby building is unlikely to be a clever solution if the journey is essentially unchanged.

The rule looks at substance, not the name on the door. New building, same commute is usually not much of a tax plan.

What About Travel from the Home Country?

For inbound employees, travel between the employee’s normal home country and the UK needs separate consideration. There are specific rules that can give relief for journeys between the normal home country and the UK workplace, including some family travel, where the conditions are met.

These rules are separate from the ordinary temporary workplace rules. That matters because advisers often try to push everything through the 24-month rule. That is not always the right answer. Home-country flights, home leave and arrival/departure journeys should be reviewed separately.

From 6 April 2025, the old non-dom remittance basis was replaced by the new foreign income and gains regime for qualifying new residents. The inbound travel rules were also updated. So older commentary referring to non-domiciled employees and the old remittance basis needs to be read carefully.

What About Short-Term Business Visitors?

Do not confuse the 24-month rule with short-term business visitor relief. They are different things. The 24-month rule is about whether travel and accommodation costs can be treated as relating to a temporary workplace. Short-term business visitor treatment is usually about whether the employee’s UK employment income is exempt under a double tax treaty, often because they spend limited time in the UK and remain employed overseas.

A person can fail the short-term business visitor test but still get temporary workplace relief. A person can also be treaty-exempt but still fail the expense analysis.These are related, but they are not the same test. For short-term business visitors, the important points usually include:

- Which country the employee is tax resident in

- The exact wording of the relevant double tax treaty

- Whether the 183-day test is measured by:

- Tax year

- Calendar year

- Any rolling 12-month period

- Who the real employer is in substance

- Whether the UK company bears the cost

- Whether salary or benefits are recharged to the UK

- Whether the UK host controls the employee’s work

Accommodation can be particularly awkward. If the UK company pays for a flat, that benefit may create a UK tax issue even where the salary remains paid overseas, unless the overseas employer ultimately bears the cost. Do not assume that “under 183 days” solves everything. It does not.

Employer Reimbursements and Payroll

Where the employee personally pays a deductible expense, they may claim tax relief. Where the employer pays or reimburses the cost, the question becomes whether the payment can be made tax-free through payroll. Since 6 April 2016, the key rule is the exemption for paid or reimbursed deductible expenses. In broad terms, if the expense would have been deductible for the employee, the employer can usually reimburse it without tax or NIC, provided the conditions are met. This includes:

- Appropriate checking

- No salary sacrifice

This is why old references to “dispensations” should be treated with caution. The old dispensation regime has gone. Some HMRC examples are still useful on the underlying tax treatment, but the payroll mechanics have changed. For globally mobile employees, employers also need to consider section 690 PAYE apportionment where the employee works partly in and partly outside the UK.

From 6 April 2025, the old direction process was replaced by a notification process. This matters where the employee has:

- UK workdays

- Overseas workdays

- Tax equalisation

- Split duties

Relocation Costs Are a Separate Issue

Not every cost should be squeezed into the 24-month rule. If the employee genuinely relocates because of a change in employment, the relocation expenses rules may be more relevant. These rules can exempt certain qualifying moving costs, subject to the £8,000 limit. That is a different regime from temporary workplace relief. A sensible file should separate:

- Arrival travel

- Temporary accommodation

- Ongoing rent

- Home-country trips

- Local commuting

- Subsistence

- Incidental overnight expenses

- One-off relocation costs

- Family costs

- Utilities and furniture

Treating all of these as one big “assignment cost” is how mistakes happen.

Practical Examples

Example 1: Genuine 18-Month Secondment

An employee works for an overseas employer and is sent to the UK for 18 months. They will return to their overseas role afterwards. They rent a modest UK flat near the workplace. The employer reimburses rent, utilities and travel. This is the cleanest case. If the UK role is genuinely temporary and the expected period is under 24 months, there is a strong case for temporary workplace relief. Rent, utilities and travel may qualify if they are reasonable and properly evidenced.

Example 2: 18 Months Becomes 28 Months

The same employee is originally sent for 18 months. After 10 months, the assignment is extended to 28 months. Relief should normally be available up to the date the expectation changes. From that date, the UK workplace may become permanent and the tax-free treatment should stop. The extension date is critical. Document it.

Example 3: Two Back-to-Back Contracts

An employee has an 18-month project at a UK site. A second project is then agreed at the same site. The first 18 months may qualify if the original expectation was genuinely under 24 months. But once the second contract means the employee is expected to exceed 24 months at that site, relief is likely to stop. A new contract does not automatically mean a new workplace.

Example 4: 12-Month UK Local Contract

An employee is hired on a 12-month UK contract to work only at one UK office. This is high risk. Even though the contract is under 24 months, the UK office may be a permanent workplace from day one because the whole employment is based there. In that case, home-to-office travel is ordinary commuting, and UK rent is normally a private living cost.

Example 5: Nearby Office

An employee works 18 months in one City office, then 22 months in another office nearby. If the commute is essentially the same, the two locations may be treated as one workplace. Relief may therefore be denied once the overall expected attendance exceeds 24 months. Changing the address is not enough. The journey must genuinely change.

Example 6: Family Accommodation

An employee on an 18-month UK secondment rents a large family house because their spouse and children come with them. The whole rent may not qualify. Relief should normally be limited to the reasonable cost of accommodation needed for the employee’s work assignment. The family uplift may be taxable.

Example 7: Expensive Location Chosen Privately

The employee works in Exeter but chooses to live in Salcombe for lifestyle reasons and then commutes. HMRC is unlikely to accept the extra rent and travel as business costs. Relief would normally be limited to what reasonable accommodation near the workplace would have cost. Private choice is not business necessity.

Example 8: Short-Term Visitor with UK-Paid Accommodation

An overseas employee visits the UK for fewer than 60 workdays. They remain on overseas payroll, but the UK company pays for a flat. The salary may be covered by short-term business visitor arrangements, depending on the treaty and facts. But the accommodation benefit may still create a UK tax problem if the UK host bears the cost. Salary and benefits must be reviewed separately.

Example 9: Flights Home

A non-resident or qualifying new resident employee receives reimbursed flights between their normal home country and the UK. Specific inbound travel rules may give relief, provided the statutory conditions are met. There is no simple assumption either way. The payment must genuinely relate to qualifying travel, not just be a general allowance.

The Main Compliance Risks

The biggest mistake is treating “under 24 months” as a safe harbour. It is not. The file needs to prove three things:

- The workplace is genuinely temporary

- The expected duration is no more than 24 months

- There is no fixed-term appointment problem that makes the workplace permanent from the start

HMRC will look at:

- The assignment letter

- Employer communications

- Project plan

- Visa paperwork

- Budget approvals

- Extension documents

If those documents tell different stories, the tax position becomes weak.

The second major risk is failing to change payroll treatment when the facts change. If an assignment is extended beyond 24 months, relief may stop immediately from the date the expectation changes.

The third risk is treating rent too casually. Rent can qualify in the right case, but not where:

- The workplace is permanent

- The property is excessive

- The location is chosen for private reasons

The fourth risk is confusing domestic temporary workplace relief with treaty-based short-term business visitor treatment. They are not the same.

‣ Is the employee genuinely seconded from an overseas employment, or have they simply been hired for a short UK role?

‣ What did the employer and employee expect at the start?

‣ Is the expected UK attendance 24 months or less?

‣ Will the employee spend 40% or more of working time at the UK workplace?

‣ Is the UK workplace the whole purpose of the employment?

‣ Could the fixed-term appointment rule make the workplace permanent from day one?

‣ Have there been extensions, renewals or second phases?

‣ Has the employee moved to a nearby workplace with essentially the same commute?

‣ Are the accommodation costs reasonable?

‣ Is there any family or private lifestyle element in the rent?

‣ Who pays the cost: employee, overseas employer or UK host?

‣ If the employer reimburses the cost, does the section 289A exemption apply?

‣ Are home-country flights covered by the separate inbound travel rules?

‣ Is the employee also being treated as a short-term business visitor?

‣ Does the relevant treaty actually support that treatment?

‣ Is there a UK recharge or economic employer issue?

‣ Does section 690 payroll apportionment apply for UK and non-UK duties?

‣ Has the position changed since 6 April 2025 because of the new foreign income and gains regime?

The Practical Conclusion

The 24-month rule can be very valuable for internationally mobile employees. Used correctly, it can allow relief for significant costs such as:

- UK rent

- Travel

- Utilities

- Subsistence

But it is not a loophole and it is not automatic. The safest cases are genuine secondments, properly documented from the start, where the employee remains part of a wider overseas employment and is expected to return after a defined UK assignment. The weakest cases are short UK contracts where the employee’s entire job is to work at one UK location. Those can be permanent workplaces from day one, even if the contract is only 12 or 18 months. So the simple rule is this:

Do not ask only: “Is it under 24 months?” Ask: “Is this genuinely temporary?”

That is the question HMRC will ask. And if the paperwork does not answer it clearly, the tax relief may disappear faster than the employee’s London rent budget.