The UK’s New Foreign Income and Gains (FIG) Regime: Ultimate Guide

From Non-Dom to FIG

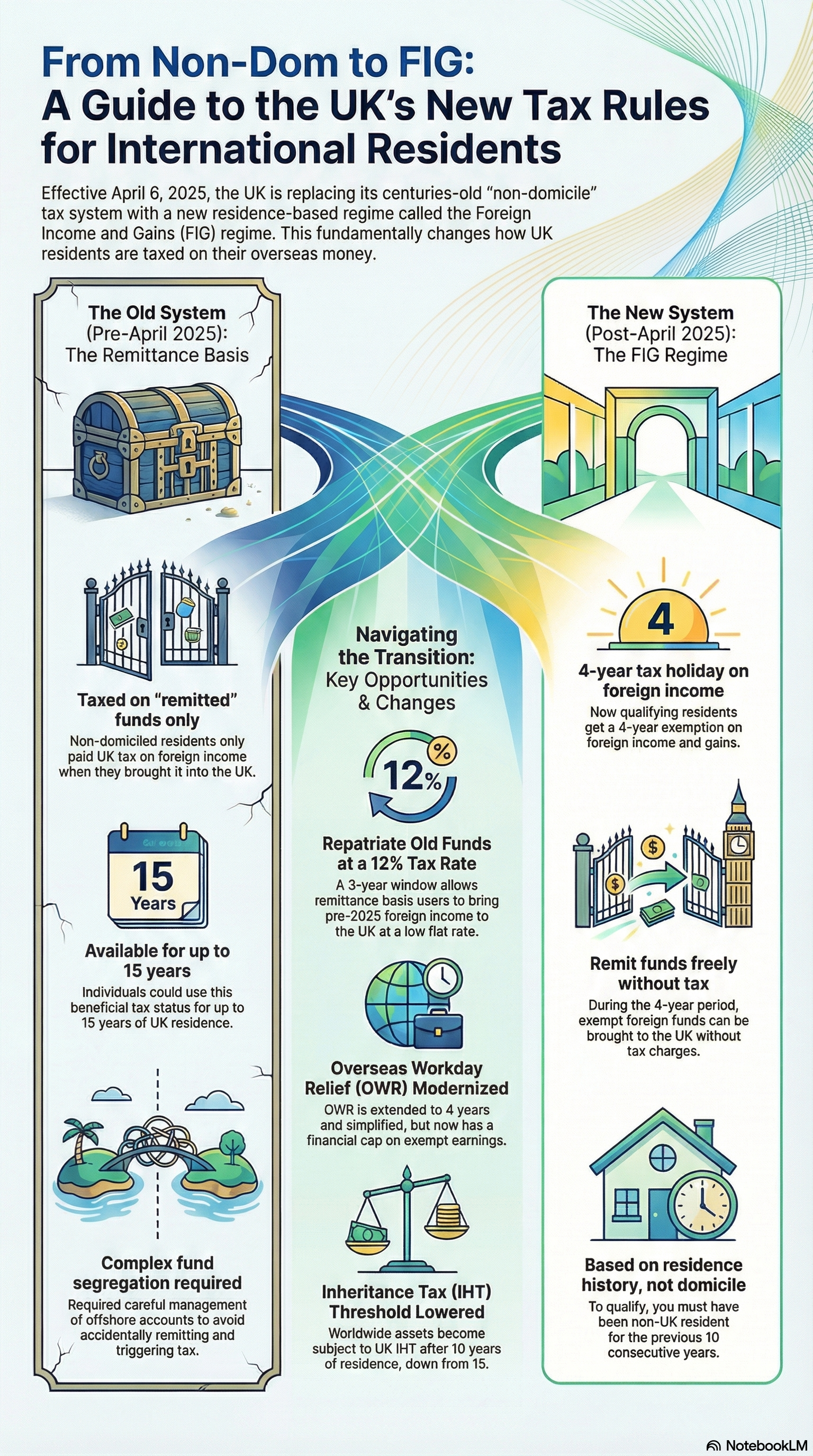

For over a century, the UK’s tax system distinguished between UK-domiciled and non-domiciled individuals (“non-doms”) for taxing foreign income and capital gains. Non-doms who became UK residents could opt for the remittance basis, paying UK tax only on foreign income or gains when “remitted” (brought into or enjoyed in the UK). This regime, while attracting international talent and wealth to the UK, drew criticism as unfair and outdated. In late 2024, the government announced the abolition of the non-dom remittance basis regime, effective from 6 April 2025.

Starting 6 April 2025, all UK residents are by default taxed on the arising basis – meaning worldwide income and gains are subject to UK tax as they arise, regardless of domicile. To soften the impact on internationally mobile individuals and continue attracting talent, a new Foreign Income and Gains (FIG) regime was introduced. The FIG regime essentially provides a time-limited exemption for qualifying newcomers on their foreign income and gains, replacing the indefinite remittance basis with a shorter, residence-focused relief. In parallel, domicile status was removed as a factor for UK tax on income, gains, and even inheritance tax, moving the UK firmly to a pure residence-based tax system.

Key policy goals: The FIG regime aims to simplify compliance (no need to keep untaxed income offshore or track remittances) while addressing fairness concerns by limiting the duration of tax breaks. It is a compromise that maintains UK competitiveness for expatriates and returning Britons but ensures that after a few years everyone pays tax on worldwide income.

Autumn Budget 2024 Implementation: The change was legislated in Finance Act 2025. The FIG system largely adopted a proposal developed under the prior government (Sunak administration) and finalised by the incoming government. Below we detail the new rules effective from April 2025, covering FIG eligibility, tax treatment, transitional provisions (rebasing and temporary low-tax remittance), Overseas Workday Relief changes, inheritance tax reform, and trust implications. We also include worked examples to illustrate the impact on different individuals, and end with a practical action plan for advisers.

For brevity, this guide focuses on individuals. The impact on offshore trusts is summarized briefly, but due to complexity a separate detailed trust guide is recommended.

Qualifying for FIG

Who can use the FIG regime? The FIG relief is available only to “qualifying new residents” (QNR), defined by a strict residence history test. To qualify, an individual must not have been UK tax resident for at least 10 consecutive tax years immediately before the year of arrival. In practice, if you move to the UK after a 10-year absence (or have never lived in the UK before), you meet this condition. This applies equally to non-UK-domiciled individuals and UK domiciled returnees – domicile status and previous non-dom tax history are irrelevant for FIG eligibility. Even British citizens who kept their UK domicile but lived abroad for over a decade can qualify, whereas a non-dom who lived in the UK more recently cannot.

Relief period – four years: Once eligible, the FIG regime can be claimed for a maximum of four consecutive tax years, starting with the tax year you become UK resident. These are typically the first four years after arrival. After this, the FIG benefits cease – no extensions beyond year 4. This is a major shift from the old regime, which allowed non-doms to use remittance basis for up to 15 years (until deemed domicile).

Transitional entry for recent arrivals: Individuals who moved to the UK just before April 2025 can still benefit for the remainder of a four-year window. If on 6 April 2025 you have been UK resident for less than 4 years and you had the requisite 10-year non-residence before your arrival, you may claim FIG for the balance of your four years.

Who cannot claim FIG: If you have not been absent for 10 years, you cannot use FIG at all, even if you were a non-dom. For instance, someone who was UK resident any time in the last decade before 2025 will be taxed on worldwide income from 2025 onward with no special relief. Additionally, Members of Parliament (House of Commons or Lords) are barred from claiming FIG, aligning with rules that previously prevented MPs from using the remittance basis.

Determining “not UK resident for 10 years”: This is assessed via the Statutory Residence Test (SRT) – the same test that determines if you are UK resident in a given year. Essentially, you must have been non-resident under SRT for each of the 10 full tax years preceding your arrival year. Special cases:

- If you arrive or depart partway through a tax year and that year is treated as a split year under SRT, the year still counts as a year of residence for FIG purposes. So partial years in the UK count fully toward the 4-year FIG limit, and conversely a split year of departure still counts as a year outside for the 10-year lookback.

- If a double tax treaty deems you resident in another country even while SRT says UK-resident, that year still counts as UK residence for FIG eligibility. In short, only actual non-residence under UK law counts toward the 10-year gap.

Breaks in the 4-year period: The four FIG years must be consecutive tax years. If you leave the UK during your FIG period and become non-resident for a year, you do not get to pause or restart the clock – the clock keeps ticking. You can resume claiming FIG if you return before the 4-year window expires, but you lose any years you were away.

Essentially, the FIG window runs from your arrival and lasts four continuous UK tax years; time out of the UK during that span just wastes part of the relief period.

Timeline of Key Dates (FIG Regime and Transitional Measures):

- Autumn 2024: Abolition of non-dom regime announced; FIG regime confirmed to begin April 2025.

- 5 April 2025: Last day of remittance basis availability. Non-doms prepare for new rules.

- 6 April 2025: FIG regime takes effect. Domicile ceases to be relevant for income/CGT; nearly all UK residents now taxable on worldwide income/gains (unless FIG claimed).

- 6 April 2025 – 5 April 2029: First cohort of FIG-eligible arrivals (those arriving 2025–26) can claim up to four years of FIG relief (2025–26 through 2028–29).

- 6 April 2025 – 5 April 2028: Temporary Repatriation Facility (TRF) window for remitting pre-2025 untaxed foreign income/gains at reduced rates (see TRF section). 12% rate applies in 2025–26 and 2026–27; 15% in 2027–28. TRF designations must be made by 5 April 2028.

- 6 April 2028: FIG regime Year 4 ends for those who arrived in 2024–25 and were eligible (they would have used FIG for 2025–26 through 2027–28).

- 6 April 2029: FIG regime Year 4 ends for 2025–26 arrivals. From 2029–30 onward, these individuals are fully taxable on worldwide income/gains.

- Mid-2030s: Inheritance Tax (IHT) “long-term resident” status begins to affect FIG users who remain in the UK. Those who arrived April 2025 and stay continuously will hit 10 years of residence by 2034–35, at which point their worldwide estate becomes subject to UK IHT (see IHT section).

Income Tax and Capital Gains Tax Treatment

Under the FIG regime, foreign income and foreign capital gains arising during the four-year qualifying period can be exempt from UK tax, provided you claim the relief. In practice, a successful FIG claim means you do not pay UK tax on the elected foreign income/gains for that year, and crucially it no longer matters whether you remit those funds to the UK or not. This is a departure from the old remittance basis where keeping untaxed income offshore was essential. Under FIG, if the income/gain is relieved, you are free to use or bring it into the UK without triggering any UK tax.

How to claim: FIG relief is not automatic – you must actively claim it each year via your Self Assessment tax return. A claim is made by identifying the foreign income and/or gains to be relieved in the tax return. The claim for a given tax year must be filed by the normal amendment deadline (31 January, nearly two years after the end of that tax year). For example, a claim for 2025–26 must be submitted by 31 January 2028. You can choose each year whether to claim and on which sources. Notably, you can claim on foreign income, or foreign gains, or both, independently – and even on a subset of sources while excluding others. This flexibility means you might exclude certain income if claiming relief on it would cause adverse consequences overseas or if it’s very small. Any foreign income/gains for which you don’t claim FIG will simply be taxed on the arising basis (with double tax relief as appropriate).

Reporting requirements: Even if FIG exempts the tax, you must report the amount of foreign income/gain being relieved in the return. Essentially all UK residents now need to report worldwide income and gains from 2025–26 onward, even if some are not taxed due to FIG. The only minor exception is if you have no UK tax liability and otherwise aren’t required to file a return, e.g. if your foreign income is extremely small and fully covered by allowances – but if you owe any tax or want to claim FIG, you must file. This is an important compliance change: previously, non-doms did not have to report foreign income kept offshore when using the remitance basis of taxation. That is not the case anymore.

Tax benefits of FIG: If a FIG claim is made, the specified foreign income and/or gains for that year are fully exempt from UK Income Tax or CGT. There is no charge or fee for claiming FIG (unlike the old remittance basis charge after 7 years) other than the loss of personal allowances (see below). Additionally, bringing the money to the UK has no UK tax impact – no remittance tax and no need for complex segregation of funds. In effect, FIG provides a tax holiday on foreign earnings for up to four years: a newcomer can earn dividends or sell assets abroad without UK tax during that period (subject to some exclusions noted below). This can result in substantial tax savings, especially for high-earners or large capital gains in those early years.

Trade-offs – loss of allowances and reliefs: To prevent double benefits, using FIG comes with similar trade-offs as the remittance basis did. If you claim FIG for any foreign income or gains in a tax year, you lose entitlement to:

- The personal Income Tax personal allowance (£12,570 at the time of writing),

- The Blind Person’s Allowance (if applicable),

- Any Marriage Allowance or Married Couple’s Allowance transfer/reduction, and

- The Capital Gains Tax annual exempt amount (£3,000 in 24/25).

These are forfeited for the whole tax year even if the FIG claim was only on gains or only on a portion of income. For instance, claiming FIG to exempt a capital gain means you still lose your personal income allowance that year, and vice versa. Therefore, FIG is not always beneficial for those with modest foreign income – you need to weigh the tax saved on foreign income/gains against the extra tax you’ll pay by losing the tax-free allowances. If foreign income is small (under allowances), you might be better off not claiming FIG so as to keep your personal allowance. One should “run the numbers” to decide the optimal choice.

No foreign loss relief: Any foreign income losses or foreign capital losses arising in a FIG-claim year cannot be deducted or carried forward for UK tax purposes. The bar applies regardless of whether you claimed on income vs gains. For example, a loss on an overseas rental property in a FIG year is not usable against other income. Thus, if you expect foreign losses (or want to preserve capital loss allowances), it may influence whether to claim FIG in that year.

Excluded income/gains: Most types of foreign income and gains qualify for FIG relief, with a few notable exceptions. One important exclusion is gains on offshore life assurance/bond policies, which are not treated as foreign income for FIG purposes. Even during your FIG period, chargeable gains from an offshore investment bond remain taxable on the arising basis (though time apportionment relief can reduce the taxable gain based on non-resident years). This exclusion is significant because offshore bonds are common vehicles for expats; be aware that their gains won’t enjoy FIG exemption. In that it's similar to what was happening under the previous non dom regime. Other exclusions include certain income that is always UK-taxable even if foreign-sourced (for example, UK government securities for UK residents, or disguised remuneration anti-avoidance income – these still get taxed). Always check HMRC’s list of qualifying vs. non-qualifying income sources under FIG.

Effect on other calculations: While FIG-relieved amounts are removed from your taxable income/gains, they are still considered for some threshold calculations. FIG deductions do not reduce your “adjusted net income” when determining things like the tapering of personal allowance above £100k, the High Income Child Benefit Charge, or eligibility for tax-free childcare. In other words, for those specific calculations, HMRC will add back the FIG-exempt income to see if you cross the limit. However, FIG income does not count as taxable income for applying tax rates or the dividend allowance, etc. This nuanced treatment means a FIG claimant with high foreign income could still lose their personal allowance due to income > £100k (since FIG doesn’t protect that), but they were losing the allowance anyway by making the FIG claim. The main point is to be mindful that FIG doesn’t help avoid those “cliff-edge” income thresholds for other rules.

After FIG period ends: Once your four years are up (or if you choose not to claim in any given year), you are taxed like any other UK resident on worldwide income. For former non-doms, note that the automatic £2,000 unremitted income exemption is gone from 2025. Even small amounts of foreign income beyond that must be reported and taxed (though you might have relief via personal allowance or savings/dividend allowances). If you plan to stay in the UK beyond the FIG window, ensure you have robust record-keeping and plans for global income reporting, and consider longer-term tax strategies (like legitimate deferral or using available treaty benefits) once full exposure kicks in.

Overseas Workday Relief (OWR) Changes

Overseas Workday Relief is a special relief for employment income, historically available to non-domiciled employees who spend some time working outside the UK in their early years of UK residence. Under the old rules, OWR could shelter foreign workday income (earnings for duties performed overseas) from UK tax for up to three years, provided those earnings were paid and kept offshore (not remitted) and certain conditions were met. With the abolition of the remittance basis, OWR has been retained and modified as part of the FIG regime, with extended duration but new limits.

FIG linkage: From April 2025 onward, OWR is only available to individuals who are eligible for (and opt into) the FIG regime. In other words, you must meet the 10-year non-residence test and claim FIG relief to use OWR. New arrivals who don’t qualify for FIG (because they were recently UK resident) cannot claim OWR at all after 6 April 2025. This ties OWR to the same four-year window as FIG.

Extended to four years: OWR can now be claimed for up to four consecutive tax years (previously three years) for qualifying individuals. Essentially, it aligns with the FIG period: years 1–4 of UK residence. For example, an eligible employee arriving in July 2025 can claim OWR for 2025–26 through 2028–29 (provided they claim FIG in those years). This extra year of relief makes the UK slightly more attractive for short-term assignments, giving expatriate employees a bit more time of tax break on their foreign workdays.

No more remittance requirement: A major simplification is that under FIG, the old requirement to keep overseas earnings unremitted no longer applies. Employees and employers no longer need to segregate pay between UK and non-UK accounts or worry about accidental remittances. Relief is granted regardless of where the salary is paid or used, as long as it’s attributable to non-UK workdays and claimed under FIG. This removes a significant administrative burden (no more complex payroll routing or monitoring of funds). Essentially, during the FIG years, one can freely bring their full salary into the UK without losing OWR relief on the foreign portion.

Simplified bank account rules: Previously, claiming OWR in practice meant structuring separate bank accounts (one for UK earnings, one for offshore earnings to avoid mixing) and strict tracking. The new rules eliminate this complexity. Employers can pay the individual’s total salary in one account if desired; the portion corresponding to overseas workdays can still be exempted via FIG/OWR, and remittance of it isn’t taxed. This is a welcome change for HR and payroll departments handling expats.

New cap on relief: To prevent abuse, the FIG reforms introduced a cap on the amount of earnings that can benefit from OWR each year. The exempt overseas workday income is limited to the lower of 30% of total employment income or £300,000 per tax year. In practice, this means high-earning employees can only shield a portion of their salary. For example, if someone earns £1 million and 50% relates to overseas workdays, previously they might have exempted £500k via OWR; under the cap, they can only exempt up to £300k (since 30% of £1m is £300k, which is the cap). Conversely, if someone earns £200k with 50% abroad (£100k overseas duties), 30% of £200k is £60k, so they can only exempt £60k out of the £100k overseas portion – effectively they’ll pay UK tax on £40k of what was foreign work income due to the cap. Important to note that the cap is annual; it resets each tax year and is applied per individual.

Interaction with personal allowance: Note that claiming OWR requires opting into FIG, which (as discussed) means giving up the personal allowance and CGT exemption for that year. For many highly paid employees, the personal allowance was already phased out by income, but mid-level earners should consider whether OWR’s benefit outweighs the loss of the allowance.

Transitional rules for current OWR users: Employees who were already in the midst of an OWR period as of April 2025 get special treatment:

- If an employee’s first OWR year was 2023–24 or 2024–25 (i.e. they arrived in 2023 or 2024), they can continue to claim OWR for a full three years under the old rules, even if they don’t qualify for FIG. This means someone who arrived in 2023–24 can still use OWR in 2023–24, 2024–25, 2025–26 (three years) without the new cap and under remittance conditions. If they do qualify for FIG (say they did have 10-year absence), they can actually extend to a fourth year under FIG (2026–27). Essentially, no one currently benefiting from OWR will lose out on expected relief – they either finish their 3 years as originally planned or get a bonus year if eligible.

- The cap does not apply to OWR claims covering pre-2025 years. So an arrival in 2023 can get OWR for 23–24, 24–25, 25–26 without the £300k/30% cap on those years. If they qualify for an extra 4th year (26–27) under FIG, presumably the cap would apply for that 4th year since it’s post-April 2025.

- Anyone arriving from 2025–26 onward who does not qualify for FIG cannot claim OWR at all. So OWR is effectively off the table for new residents unless they meet the 10-year non-res test.

Practical implications: From an employer perspective, these changes may make the UK more appealing for expatriate assignments:

- Longer relief period: Four years gives slightly more flexibility in planning assignment lengths and potential tax savings.

- Administrative ease: Removing the remittance requirement and separate account structure simplifies payroll and assignee financial planning.

- Plan around the cap: Employers might need to consider structuring compensation (e.g. use of bonuses, equity, etc.) or timing to maximize use of the £300k/30% OWR cap. Extremely high earners likely will pay some UK tax even on overseas duties due to the cap, so projections should account for that.

- NI contributions: Note that OWR (old or new) does not relieve UK National Insurance contributions – it only affects income tax. If an employee is working for a UK employer, NI may still be due on full pay unless they’re on an overseas social security scheme via detached duty rules.

Overall, OWR remains a valuable relief for internationally mobile employees, now integrated into the FIG system. It provides an initial period of tax-efficient income for global workers, albeit now with a quantitative cap. Both employees and employers should adjust to the new “claim-based” process and cap – e.g., ensuring that claims are made in tax returns and keeping evidence of days spent working abroad to support the OWR portion if needed.

Rebasing Relief for Former Non-Doms

One concern with ending the remittance basis is how to tax unrealised capital gains that accrued offshore in the past. Many non-doms hold assets that have appreciated over years or decades. Under remittance rules, gains on foreign assets realized while non-dom could often be kept offshore without UK tax. Now that such gains will become taxable on an arising basis once the individual is within scope, the government offered a one-time “rebasing” relief for certain individuals, to avoid taxing historical growth that occurred before the new regime.

Rebasing to 5 April 2017: Eligible individuals can elect to reset the tax basis of their foreign assets to the value as of 5 April 2017 for UK CGT purposes. This means that only the gain arising from 5 April 2017 onward would be subject to UK tax when the asset is eventually sold (any growth prior to that date is effectively wiped out for UK tax). Why 2017? This date aligns with the last major non-dom reforms (in April 2017, the deemed domicile 15-year rule came in, and a rebasing was offered to those becoming deemed domiciled then). The government chose to use the same valuation date to simplify things – effectively extending that 2017 rebasing opportunity to a wider group now in 2025.

Who can rebase assets? The conditions for rebasing relief are strict:

- The individual must never have been UK domiciled (under general law) nor deemed domiciled in the UK before the 2025–26 tax year. In essence, true non-doms who haven’t yet spent more than 15 out of the last 20 years in the UK by April 2025.

- They must have claimed the remittance basis in at least one tax year between 2017–18 and 2024–25. (Years where the remittance basis applied automatically due to <£2,000 unremitted are ignored; they need an actual claim). This indicates the relief is targeted at those who actively used the non-dom regime recently.

- The asset in question must have been owned by the individual on 5 April 2017 and still held until a sale on or after 6 April 2025.

- The asset must have been located outside the UK throughout 6 April 2024 to 5 April 2025 (the year before FIG starts). This prevents someone from bringing an asset to the UK and then trying to use rebasing on it.

If all conditions are met, the individual can elect to treat the asset’s base cost for CGT as its market value at 5 April 2017. This election can save significant tax for assets that grew in value before 2017.

Use with FIG: If an individual is also eligible for FIG and sells a foreign asset during their FIG 4-year period, they actually don’t need rebasing – because any gain on that sale would be fully exempt under FIG relief (assuming they claim the foreign gain relief). Rebasing is more relevant for assets that will be sold after the FIG period or by individuals who don’t qualify for FIG but meet the rebasing criteria. For example, a long-standing non-dom who is now taxed on arising basis from 2025 (not FIG-eligible because they didn’t have 10-year break) might use rebasing to shield pre-2017 gains on assets they sell in, say, 2026.

Reminder: This rebasing applies only to foreign assets. UK-sited assets were always taxable for residents and had no remittance protection, so there’s no rebasing for UK assets.

Avoid mingling old gains with principal: A practical caution – if you sell a foreign asset after April 2025 that you owned prior, be careful when remitting the proceeds. The sale proceeds could contain “tainted” money: original capital, rebased untaxed gain, etc. If an asset was originally bought with untaxed foreign income/gains under remittance basis, bringing the sale proceeds to the UK could trigger a tax charge on that original untaxed income if not handled correctly. The Temporary Repatriation Facility (TRF) (discussed next) may allow you to bring such funds in at a lower rate by designating them. Without TRF, the mixed fund rules would apply to any remittance, potentially taxing the portion of proceeds attributable to pre-2025 income or gains used to purchase the asset. In short, rebasing doesn’t automatically make remittances tax-free – it just steps up the base for CGT calculation. One must still consider if any part of the money they bring in represents previously untaxed income/gain (which could be taxable or require TRF designation).

Two separate rebasing reliefs: Note that an earlier rebasing relief was offered in 2017 for those who became deemed domiciled then. The new 2025 rules keep that 2017 rebasing option in place and extend availability such that eligible taxpayers in 2025 don’t need to maintain non-UK domicile status beyond April 2025 to use it. Practically, this means if someone would have qualified for 2017 rebasing but didn’t become deemed dom until now, they can still use the 2017 value. Taxpayers and advisers must be careful to identify which rebasing relief they are using and ensure all conditions are met. Documentation of 5 April 2017 market values will be crucial. If values weren’t documented at the time, consider obtaining retrospective valuations to support any future computation.

The Temporary Repatriation Facility (TRF)

One of the most significant transitional measures is the Temporary Repatriation Facility (TRF). This is a time-limited opportunity (3 years) for individuals who had previously accumulated untaxed foreign income or gains (under the remittance basis) to bring those funds into the UK at a reduced, flat tax rate. It’s designed to encourage non-doms to “repatriate” offshore money under favorable terms, rather than leaving it offshore or facing full UK tax if remitted under normal rules.

What funds qualify? TRF applies to foreign income and gains that arose before 6 April 2025 while the individual was on the remittance basis. This includes:

- “Stockpiled” foreign income or capital gains that were earned/accrued in years up to 2024–25 and were never taxed in the UK (because they weren’t remitted).

- It can also apply to mixed funds (accounts containing mixtures of income/gains from various years and clean capital) – normally very complicated to remit, but TRF simplifies this (as explained below).

In essence, if you have money sitting abroad that would trigger a UK tax charge if you bring it in now (because it’s not clean capital), you can choose to “designate” an amount of those funds under TRF and pay a low flat-rate tax to cleanse them.

Eligibility for TRF: Not everyone can use TRF. You must meet two key conditions:

- Claimed remittance basis between 2017–18 and 2024–25: You need to have been a remittance basis user in at least one of the recent tax years. If you never claimed (for example, if you were always on arising basis or became deemed dom long ago), you’re not the target of this relief.

- Not UK-domiciled or deemed domiciled before 2025–26: You must not have become deemed domiciled prior to April 2025 (i.e. not a 15-year long-termer) and not have been UK domiciled in that period. Essentially current non-doms who are now losing the regime qualify, but if you already lost non-dom status earlier, you likely can’t use TRF.

This typically includes many non-doms who were under 15 years in UK by 2025, or who might have left before reaching 15 years and are now returning.

TRF time window and tax rates: The facility is only open for three tax years: 2025–26, 2026–27, and 2027–28. The applicable flat tax rate on designated amounts is:

- 12% for designations made in 2025–26 or 2026–27,

- 15% for designations in 2027–28.

After 5 April 2028, TRF closes – any unremitted funds will face normal tax rules if remitted (usually taxed at full Income Tax or CGT rates up to 45%/20% etc.). So it’s a use-it-or-lose-it opportunity.

The rate is the same regardless of whether the funds are income or capital gains, etc., and there are no additional taxes on remittance once this charge is paid. Notably, 12%/15% is a substantial discount compared to top marginal rates (e.g. 45% Income Tax or 20%/28% CGT) – it’s even lower than the basic tax rate. This could be very attractive to those with large untaxed sums abroad.

How it works (designation process):

- The individual decides an amount of their offshore funds to “designate” for TRF in a given year. This is done through the Self Assessment tax return – you will include a designation and calculate the TRF charge due.

- The TRF tax (12% or 15%) is payable on the designated amount at the time of designation, not when you actually transfer the money. You could designate funds you plan to remit in the future – pay the low tax now, and then remit later when convenient.

- Once designated and the TRF charge paid, those funds (now considered “designated FIG”) can be brought to the UK any time thereafter (even in a later year) with no additional tax. There’s no need to declare the actual remittance when it happens, as long as it doesn’t exceed what was designated.

- You do not need to trace every source of income/gain in a mixed fund for TRF. TRF allows you to simply pick a round amount from an account. When you later remit, the rules will treat the designated amount as coming out first (before any other untaxed components). This overrides the normal “mixed fund ordering” rules which are notoriously complex.

Simplification of mixed funds: Under normal rules, if an offshore account contains multiple years’ income, gains, and clean capital, any transfer out has to be dissected in a strict order (current year income first, then last year income, etc.), potentially leading to higher tax. TRF changes this:

- If you designate an amount in a mixed account, that amount will be treated as the first money out on any remittance, regardless of the usual ordering. So you effectively mark a portion as “cleaned” by paying 12/15% on it, and when you transfer money, it uses that portion first. It's the easiest way to create clean capital from mixed funds.

- Additionally, when analyzing multiple remittances and transfers in a year, you can aggregate them for simplicity and treat as if one big remittance at year-end. This avoids transactional analysis for each movement.

Scope of TRF for trust-related funds: Initially, there was debate whether trust distributions would qualify. The final policy does allow TRF to apply in some trust scenarios:

- If a non-dom beneficiary received a trust capital payment before 6 April 2025 that was not taxed (because of remittance basis), they can designate that under TRF when bringing it in.

- If a beneficiary receives capital payments during 2025–26 to 2027–28, and those payments are matched to pre-2025 trust income/gains, they can use TRF (provided the beneficiary had claimed remittance basis in a prior year).

- However, trust income distributions on or after 6 April 2025 do NOT qualify for TRF even if sourced from old income. Only capital payments do, which is an anti-avoidance measure (so one cannot simply relabel an income distribution as TRF-eligible; likely such distributions will be taxed normally).

In short, TRF can help folks get old trust monies out at 12/15% too, which is significant for those who set up offshore trusts.

No double tax relief or foreign tax credit: The TRF charge is a UK domestic flat tax. If the offshore income already suffered foreign taxes, no credit is given against the 12%/15% TRF charge. So one should plan designations accordingly – if some funds have high foreign tax already paid, it might not be efficient to designate those (they might be better brought in under normal rules and claim foreign credit, depending on rates). Typically, TRF is most attractive for funds that were subject to little or no foreign tax (pure untaxed income or gains in low tax jusridictions, for example).

Using TRF vs not using: If you forego TRF, any remittance of pre-2025 untaxed income would be taxed at your marginal rate (potentially 40% or 45% for income, or 20%/28% for gains). TRF offers 12–15%. For many, this is a no-brainer to use as much as the law allows. However, there may be strategic considerations:

- You might not want to bring all your money onshore – if you plan to eventually leave the UK again for good, you could keep wealth offshore and avoid UK tax entirely. TRF is mainly if you need or want to use the funds in the UK.

- Cashflow: paying the TRF tax up front in, say, 2025–26, for money you might remit in 2027, means front-loading the tax payment. But since it’s so much lower, it could still be wise.

- Capitalize on the 12% years: It’s expected many will designate in the first two years at 12% rather than wait for 15%. The law as written has 15% in the third year (2027–28), presumably to incentivize early repatriation.

- You cannot use TRF after April 2028. So if you still have untaxed funds by then, any future remittance would be full-rate taxed. Some individuals might thus choose to pre-emptively designate and pay TRF on funds they might not even immediately need, just to “lock in” the low rate for flexibility later (since once designated, you can remit anytime even after 2028 with no tax).

Process and record-keeping: HMRC does not require submission of detailed sourcing calculations with the return for TRF, but you should retain documentation of what the funds consist of and evidence that you met the conditions (e.g. proof of remittance basis claims in past, statements of accounts) in case of enquiry. Also note, paying the TRF via an offshore account counts as a remittance (unlike the old remittance basis charge which could be paid from offshore without triggering tax). So one should pay the 12% charge from onshore funds or accept that paying it from the offshore pot will use up some of that pot in a taxable way (though presumably you’d then designate that portion as well to avoid double tax).

The TRF is a one-time golden opportunity for those affected by the non-dom reforms. The government’s hope is that it will lead to a flood of money flowing into the UK economy (business investments, property purchases, etc.) that would otherwise have stayed offshore.

The Long-Term Residence Rule (IHT changes)

Beyond income and capital gains, a major reform was made to UK Inheritance Tax for non-doms, effective 6 April 2025. Previously, whether an individual’s worldwide estate was subject to UK IHT (40% death tax) depended on their domicile status. Non-doms (not domiciled in the UK) were only charged IHT on UK assets, until they became “deemed domiciled” after long residence (15 out of 20 years). Now, domicile has been removed from the equation – similar to income tax, IHT has moved to a residence-based test.

Long-term resident = IHT worldwide scope: From 6 April 2025, an individual will be subject to UK IHT on their worldwide assets once they are a “long-term resident”, defined as resident in the UK for at least 10 out of the last 20 tax years immediately before the relevant date (death or a transfer). In practical terms, an incoming person will be outside the IHT net on non-UK assets for their first 9 years of UK residence, and only from the start of their 10th year onwards do overseas assets fall into scope. This is a shorter timeline than the old 15-year domicile rule.

For example, someone arriving in 2025 who stays continuously would become a long-term resident by 2035 (10 out of 10 years), and at that point all their assets worldwide (UK and foreign) are exposed to UK IHT. If they left the UK before accumulating 10 years, their foreign assets would remain outside UK IHT.

Under-20 rule: A special tweak exists for young individuals: if someone is under age 20 at death or transfer, the test is whether they’ve been UK resident in at least half of the tax years since birth. This prevents, say, a teenager who moved to UK at age 15 from being called a long-term resident at 10 years (which could happen mathematically if they lived to age 25, 10 of 20 years, but they were only 5 when they arrived which wouldn’t align with intention). So minors have a proportional threshold.

Formerly domiciled residents: The concept of FDR (a returning UK-domiciled person) has been scrapped; domicile is simply not relevant to IHT now. Even if you were born in the UK with UK domicile and then became a domicile of choice elsewhere, under the new rules you get treated like anyone else – you have 9 years grace on foreign assets once you come back (if you had been gone 10 years to qualify for FIG, you also reset the IHT clock; if not gone that long, see transitional rules below). Conversely, a person who is UK-domiciled but lived abroad for 10+ years and then returns is initially not caught for overseas assets until they hit 10 years residence again. So in a sense, the IHT regime now mirrors FIG: a decade outside resets things.

Trailing liability (IHT “tail” after leaving): Under prior law, a non-dom who became deemed domiciled for IHT kept that status for up to 3 years after leaving the UK (the “3-year tail”). The new system introduces a variable tail depending on how long you were here:

- If you were a long-term resident for 20 or more years, the tail is 10 years after departure.

- If you were resident for between 10 and 13 years, the tail is 3 years (minimum).

- For each additional year of residence beyond 13 (up to 19), add one year to the tail, capping at 10.

This graduated approach prevents someone who only just hit 10 years from having a decade-long exposure after leaving – they only get 3 years. But someone who was here nearly permanently (20+ years) has a full 10-year tail. In any case, 10 years of non-residence resets your IHT status fully. This aligns with FIG eligibility: after 10 years away, you’re no longer a long-term resident for IHT.

Effect of the tail: If you leave the UK and die (or transfer assets to trust) within your tail period, you could still be subject to UK IHT on worldwide assets. For instance, someone resident 15 years gets a tail of 8 years; if they die 5 years after leaving, they’re still within that and UK will tax their estate worldwide. This is an anti-avoidance measure so people don’t briefly leave just to avoid IHT and come back.

Transitional rules (IHT): These rules can be complex, but in summary:

- If an individual is non-UK resident in 2025–26 and was not UK domiciled as of 30 Oct 2024 (the announcement date), then old rules apply for them until they return. So someone who left the UK before the changes doesn’t suddenly become subject to new 10-year rule retrospectively. If they weren’t deemed dom on 6/4/25, they have no tail; if they were deemed dom as of that date, they keep a 3-year tail from when they left.

- Essentially, if you left before Apr 2025, you’re governed by old domicile rules for your post-exit situation. But if you come back in future, the new rules will apply going forward.

Most of these transitional details are relevant for those who recently left or were on the cusp of deemed dom status at the time of reform.

End of excluded property based on domicile: Before 2025, non-UK assets held by a non-dom (or in trust by a settlor who was non-dom when settled) were typically “excluded property” not subject to IHT. From 2025, that concept now hinges on residence status instead. Foreign assets are excluded from IHT only if the owner is not a long-term resident (or non-resident entirely) at the relevant time. So, once you become long-term resident, your previously excluded foreign assets become chargeable (except via trust structures in the past, which now also change – see Trusts section).

Estate planning considerations: The new IHT rule essentially gives new arrivals a 9-year window where their overseas assets are not in the UK IHT net. After year 10, if still UK resident, those assets become exposed:

- This encourages planning such as foreign trusts or gifts before hitting the 10-year mark. If an individual anticipates staying long-term, they might settle foreign assets into trust or gift them away during that initial period, because once they are a long-term resident, transferring those assets later could trigger IHT or gift-with-reservation issues.

- Insurance: Those planning to remain may consider life insurance to cover the potential IHT on worldwide estate once they pass the 10-year point.

- For returning Brits or long-term expats, note that leaving the UK for 10 years “resets” the clock – some families might consider that in their long-term plans (though 10 years is a substantial move).

- Onward gifting: One transitional nuance – a gift of foreign assets by someone who isn’t yet long-term resident remains outside IHT even if they die after becoming long-term resident, as long as the gift was made while not long-term resident. Conversely, a gift made while long-term resident is in scope even if the donor later ceases to be long-term resident before death. Basically, the status at time of gift now determines if it’s potentially exempt (7-year rule still applies too).

Trusts and IHT: Previously, non-doms could settle foreign assets into an offshore trust before becoming deemed dom, and that trust would remain outside IHT even if they later became UK domiciled. That protected status is essentially going away. If the settlor becomes a long-term resident, their trust’s foreign assets likely won’t be excluded property anymore (depending on the exact timing; see Trusts section for income/gains changes, and note IHT for trusts would treat settlor as having a UK deemed domicile equivalent once long-term res). The new rules treat a company as UK resident for IHT if incorporated or centrally managed here, but that’s a minor point.

Impact on Trusts

Trust taxation under the non-dom regime was exceedingly complex, and the FIG reforms have introduced further changes. A full analysis is beyond the scope of this guide, but we highlight the key points. Specialist advice is strongly recommended for anyone with offshore trusts.

Previous regime: From 2017 to 2025, “protected trust” rules allowed non-dom settlors who became deemed domiciled to avoid UK tax on foreign income and gains within an offshore trust, as long as no additions were made and the settlor did not personally benefit. Only when trust funds were distributed to UK beneficiaries would UK tax potentially arise (and even then, non-dom beneficiaries could use remittance basis to defer tax on distributions kept offshore). These rules meant many non-doms established trusts before becoming deemed dom, to shelter growth from UK tax.

What changes in 2025: In short, those trust protections are largely removed going forward. The FIG regime and associated reforms treat trust income and gains more like they would for UK domiciles, unless the beneficiaries or settlor can themselves use FIG relief:

- Settlor-interested trusts: If the settlor is UK resident and retains an interest (broadly, can benefit or close family can benefit), then from 6 April 2025 the foreign income and gains arising in the trust (and its underlying entities) are taxable on the settlor as they arise – except to the extent the settlor can claim FIG relief. In other words, if you set up an offshore trust and are now resident, you can no longer defer UK tax on the trust’s income/gains by virtue of non-dom status. You’ll pay tax yearly on trust income (with credit for any allowable expenses) just like if you owned the assets directly, unless you are within your FIG 4-year window and choose to claim relief on that trust income/gain. This is a monumental shift – many long-term non-doms will see new tax bills on their trust portfolios post-2025.

- FIG for settlors: If a settlor qualifies for FIG (e.g. a returning settlor who was non-resident 10+ years) and claims it, then during the FIG years they won’t be taxed on the trust’s foreign income/gains as they arise. But once FIG years end, taxation kicks in fully. This effectively delays trust taxation for up to 4 years for qualifying newcomers.

- Beneficiaries’ distributions: For trust distributions (capital payments) to a UK resident beneficiary:

- If the beneficiary is FIG-eligible and claims FIG in that year, the distribution (whether income or capital in trust terms) is not taxed on the beneficiary. It doesn’t matter if the payment is brought to the UK – FIG covers it. However, that distribution also does not wash out the trust’s accumulated income/gains for future (since it’s not taxed). Normally, a capital payment to a beneficiary is matched to the trust’s stockpiled income/gains and thereby “uses them up” for tax purposes. Under FIG, the payment is ignored for matching. This means you cannot use a FIG-covered beneficiary to cleanse a trust’s taxable pools – those pools remain to potentially hit someone else later. If a FIG beneficiary fails to report a distribution, though, HMRC will treat it as a taxable match anyway, so proper disclosure is critical.

- If the beneficiary is not FIG-eligible (or doesn’t claim FIG that year), any capital payment to them will be taxed if it matches to trust income/gains, same as before. Since post-2025 most trusts won’t have “protected” status, essentially all foreign income/gains in the trust are in the matching pool. The beneficiary will pay tax when they receive payments matched to those gains/income (even if they keep it abroad, because remittance basis is gone – now just being a UK resident beneficiary triggers tax when a benefit is provided).

- Pre-2025 accumulated income/gains: Trust income and gains that arose before April 2025, if not previously taxed, remain in the trust’s pool. They will be taxed when matched to a capital payment to a UK resident beneficiary (no change there). The difference is now every UK beneficiary is taxable (no remittance shelter anymore) and settlors too as noted.

- Removal of “protected” status: In short, any non-dom or deemed-dom settlor who remains UK resident after April 2025 loses the ability to keep trust growth tax-free. The trust’s foreign income and gains will be taxable either on the settlor annually or on beneficiaries when distributed. The special shield that existed 2017–2025 is gone. Only FIG claims or (rarely) the settlor becoming non-UK resident again can stop the tax.

- Onward gifts and close family: Anti-avoidance rules were adjusted to prevent using family members with FIG to bypass tax. If a FIG-using beneficiary receives a payment and then gifts it to a UK resident within 3 years, that could trigger the original amount being taxed on the second recipient (unless they also have FIG). And if the beneficiary is the settlor’s close family (spouse or minor children) and they get a FIG-free distribution, that amount might be taxed on the settlor unless the family member also claims FIG. These rules ensure FIG isn’t exploited by routing distributions through eligible family members.

- Trusts and TRF: The TRF rules (discussed above) explicitly allow using TRF for pre-2025 trust income/gains that are matched to capital payments in the 2025–2028 period. This is aimed at beneficiaries who don’t qualify for FIG. For instance, a long-term UK resident beneficiary (not FIG-eligible) could take a distribution in 2025–26 and designate it under TRF to pay 12% rather than 45%. This is a significant planning point: families might decide to distribute sizeable trust funds in that 3-year window so beneficiaries can use TRF’s low rates. However, trust income distributions cannot use TRF at all – so if trustees want to favor TRF, they should ideally distribute out of capital (even if it carries taxable income/gains within).

- Recovery for settlor: If a settlor pays tax on trust income under these new rules (via Transfer of Assets Abroad rules), there’s a new statutory right for them to recover that amount from the trust without tax consequences. This aligns with existing rights under other trust taxation provisions. If they choose not to get reimbursed, that foregone recovery could be seen as adding funds to the trust (which might break trust protections or trigger IHT), so settlors are encouraged to actually exercise reimbursement.

In summary, offshore trusts are no longer a panacea for avoiding UK tax for resident non-doms. Many will become tax inefficient after these changes, except possibly during the settlor’s FIG period. Trust holders should seek advice: some may unwind trusts, others may accelerate distributions while TRF is available, or consider restructuring. Trusts remain useful for inheritance tax mitigation (assets in trust are outside estate if properly done before becoming long-term resident), but the income/gain tax deferral benefit has been largely removed post-2025. In a way, offshore bonds have become much more appealing from a tax perspective, as they’re among the few remaining options that allow tax-free capital growth outside of ISAs and pensions.

Examples: How the FIG Regime Affects Individuals

To illustrate the new rules, here are 3 hypothetical scenarios and how FIG and related measures would apply:

Example 1: Recent Arrival Pre-2025 – Transitional OWR and Partial FIG

John moved to the UK on 1 July 2022 for a job assignment. He was non-UK resident for 15 years prior (so he would qualify for FIG on arrival, but FIG didn’t exist yet). He claimed the remittance basis in 2022–23 and 2023–24. He also claimed Overseas Workday Relief in those years, since 60% of his workdays were abroad and his employer paid that portion of salary offshore.

By April 2025, John has been UK resident for 2.5 years (2022–23, 2023–24, 2024–25). Under old rules, he expected to continue remittance basis and claim OWR through 2024–25 (three years from arrival).

Changes from April 2025: Remittance basis is abolished, so for 2025–26 John ordinarily would be taxed on worldwide income. However, since John had a 15-year break before 2022 and has been resident less than 4 years as of April 2025, he qualifies as a “transitional FIG” case. This means he can claim FIG for the remaining part of a 4-year period starting 2022–23:

- John’s first year of UK residence was 2022–23 (year 1), then 2023–24 (year 2), 2024–25 (year 3). So 2025–26 will be year 4 of his residence. He can claim FIG for 2025–26 only (the last year of his four).

- In 2025–26, John does so – he claims FIG on his foreign dividends and interest, which amount to £50k, making them tax-free. He has no big capital gains that year, so he doesn’t use FIG for gains. Claiming FIG means he loses his personal allowance for 2025–26, but his UK salary is high (£300k) so he wasn’t getting an allowance anyway (it was phased out due to income).

- Importantly, John’s foreign salary from overseas workdays in 2025–26 can also be sheltered under OWR because he’s FIG-eligible. In fact, John was already claiming OWR since 2022. So for 2025–26, John’s overseas workdays (let’s say 60% of his time, with corresponding salary £180k paid offshore) remain untaxed in the UK. Under new OWR rules, he doesn’t need to worry about remitting it; he can bring that £180k to the UK without tax. However, the cap applies: The lower of £300k or 30% of total pay. His total pay is £300k, 30% of that is £90k, so actually only £90k of his overseas earnings are exempt, and £90k of what were foreign work earnings become taxable due to the cap. Under old rules he’d have exempted the full £180k if unremitted.

After 2025–26: John’s FIG window is exhausted after that year (4 years since arrival are up). From 2026–27 onward, he is fully taxable on everything. He can no longer use OWR either (past 4 years). Suppose he stays until 2030: by then he will have been UK resident 8 years. Under the new regime he’ll never pay a remittance basis charge (because it’s gone), but he is paying annual taxes on worldwide income. If he plans to stay longer, he’ll reach 10 years by 2032, making him IHT-exposed worldwide at that point.

TRF opportunity: John accumulated some unremitted foreign income in 2022–25 under remittance basis (bonuses, etc., sitting offshore). He has, say, £400k in a Singapore bank from pre-2025 earnings. In 2025–26, John can consider using the TRF. He qualifies (claimed remittance basis before, not deemed dom yet). He decides to designate £300k of that at 12%, paying £36k UK tax, and then brings that £300k into the UK to buy a house. The remaining £100k he leaves offshore for now. In the next year 2026–27, TRF still 12%, he might designate more if needed. By doing this, he avoids what would have been 45% tax if he remitted those funds under normal rules.

Summary: John bridged the old and new systems. He effectively got 3 years of old remittance/OWR benefits and 1 year of new FIG/OWR benefits. The cap on OWR reduced his relief in the last year, but he still saved tax. He leveraged TRF to cheaply repatriate funds earned while on remittance basis. Going forward, John must adjust to being a normal UK taxpayer on worldwide income – perhaps negotiating tax equalization with his employer or using foreign tax credits if he’s paying tax abroad on some of that income.

Example 2: Long-Time Non-Dom with Offshore Funds – Using TRF to Repatriate

Zhang is a wealthy non-dom who has lived in London since 2010 (15 years by 2025). He never acquired a UK domicile. Under old rules, he became deemed domiciled in 2025 (15 of 20 years) and would have lost remittance basis anyway then. Over the years, he kept most of his investment income offshore and did not remit gains. As of April 2025, Zhang has £5 million in various offshore accounts that represent accumulated untaxed foreign income and capital gains from 2010–2025.

With the new law, from 6 April 2025 Zhang is taxed on an arising basis (as he’s UK resident and domicile is irrelevant) – so new foreign income will be taxed going forward. But the big question is what about the £5m old money if he wants to bring it in?

TRF usage: Zhang meets TRF conditions (he claimed remittance basis in many years and wasn’t UK-domiciled or deemed dom before 2025–26, since deemed status technically starts 2025–26 for him). He has a 3-year window to bring money in at low tax:

- In 2025–26, he designates £2 million under TRF at 12%, paying £240k. He then remits that £2m to the UK to purchase a property and some UK investments – no further tax on that remittance.

- In 2026–27, he designates another £2 million, paying another £240k (12%). He doesn’t actually transfer all of it immediately, but knows he can later.

- By 2027–28, he has £1m left abroad. He considers waiting hoping for future leniency, but since TRF will rise to 15% this year and then vanish, he decides to use it one last time. He designates the remaining £1m at 15%, paying £150k. Now all £5m has been taxed under TRF and can be freely used in the UK whenever he wants.

- His total tax paid to cleanse £5m = £630k (an effective rate of 12.6% overall). Had he remitted £5m under normal rules as a higher-rate taxpayer, he could have faced ~£2 million of tax (assuming much of it was untaxed income). So he saved a huge sum by utilizing TRF.

Investments and rebasing: Zhang also owns a portfolio of stocks abroad he bought in 2005 for £1m, which by April 2017 were worth £3m, and by 2025 are worth £4m. If he sells them now (post-2025) as a UK resident, he’ll be taxed on gains. He qualifies for the rebasing relief (never UK-domiciled and had remittance basis in at least one year 17–25). If he sells in 2026, he can elect to treat the base as £3m (2017 value). So UK CGT would only apply on £1m gain (from 2017 to sale) not the full £3m gain from original cost – saving perhaps £200k in CGT. If Zhang were to leave the UK for a few years, he might even avoid CGT entirely, but assuming he stays, rebasing is useful. (If Zhang had become UK deemed-domiciled at some point before 2025, he wouldn’t get this. But he wasn’t.)

Outcome: Zhang effectively regularized £5m of offshore wealth at a low cost and brought it onshore, taking advantage of the government’s limited-time offer. He now is fully in the UK tax system for new income, but he has significant clean capital to use in the UK. He must now contend with being immediately “long-term resident” for IHT since he hit 15 years – under transitional rules, as of April 2025 he was deemed dom, so he remains exposed for 3 years after any departure (if he leaves). If he stays put, all his assets are subject to UK IHT on death. He plans to engage in estate planning (like possibly gifting or trust transfers) now that the funds are onshore and accessible.

Example 3: Returning UK Expat – FIG Benefits for a British National

Priya is a British citizen who lived in the UK until 2008. She then moved to Dubai for work and has been non-UK resident for 15 years. She retained her UK domicile of origin even while abroad. Now in mid-2025 she plans to move back to the UK with her family. Historically, Priya was not eligible for the remittance basis (because she’s UK-domiciled by origin, and the old remittance rules didn’t apply to UK doms except those with foreign domiciled parents returning, etc.). Under the new system, domicile doesn’t matter – it’s about residence history.

FIG eligibility: Priya has been non-resident 15 years, so she qualifies for FIG as a “qualifying new resident”. She can claim FIG relief for her first 4 years back (2025–26 through 2028–29). This is a big advantage she wouldn’t have had under the old regime (as a UK domiciled individual coming home, she’d have been taxed on worldwide income immediately). Now she is effectively treated the same as any other expat returning after a long period: a 4-year grace period.

Her situation: Priya has investment income from Dubai bank accounts (£30k/year) and some capital gains on a share portfolio. She also negotiates with her employer to keep a portion of her role based in Dubai for the first couple of years, meaning she will have some Overseas Workday Relief on her salary. Because she’s FIG-eligible, she can claim OWR on that foreign work income for up to 4 years (and no need to worry about remittance).

Using FIG: Priya claims FIG for:

- Foreign investment income – exempting that £30k/yr from UK tax for 4 years. She loses her personal allowance each year as a result, but her UK salary is £150k so it was phased out regardless. She saves roughly £12k tax per year by not paying on the £30k foreign income.

- Foreign capital gains – she sells some stocks in 2027 while FIG is in effect, realizing £100k gain tax-free (which would have been £20k CGT otherwise).

- OWR on employment – 2025–26: She spends 40% of workdays in Dubai, so 40% of her £120k salary (£48k) is OWR-eligible. Cap check: 30% of £120k = £36k, so she can exempt up to £36k (cap hits since £48k > £36k). So £36k of her salary is tax-free, the rest taxed. In subsequent years her overseas workdays fluctuate, but she always applies the cap. Over 4 years she gets perhaps £100k of salary exempt that she brings over freely. All this she reports properly in her returns.

- No remittance worries: Priya brings back her savings from Dubai right when she moves – this is just clean capital (past earnings already taxed in Dubai or tax-free there), so not an issue. Her ongoing Dubai-sourced earnings and gains she also freely remits since they are FIG-exempt.

IHT planning: Because Priya is UK-domiciled, one might assume her worldwide estate was always in scope. However, since she was non-resident 15 years, under new rules when she arrives she is not yet a long-term resident. In fact, she will only become one after 10 years (by 2035). So for her first 9 years back, only her UK assets are subject to IHT. Her overseas assets (say a rental property in Dubai) are protected until she hits year 10. The old rules would have counted her as UK domiciled immediately and taxed worldwide estate from day one of return because she never lost UK domicile – the new test gives her a break based on residence. She uses this window: for example, she keeps her Dubai property until year 9 and then sells or puts it in trust before year 10 to avoid it coming into IHT scope.

Outcome: Priya, despite being British and UK-domiciled, benefited from the FIG regime designed for “inpatriates.” She enjoyed several years of partial tax exemption, aiding her transition back to the UK. By year 5 onwards, she’s fully taxable, but by then her foreign income might have diminished or she’s reorganized finances. She also smartly used the time before becoming a long-term resident to structure her estate to minimize IHT.

These examples demonstrate how FIG and related measures work in practice: new and returning residents get a tax head-start, whereas long-time residents must adapt to a world of no remittance shelter (using TRF where possible to ease the pain). Each individual’s choices (what to claim, whether to use TRF, how to time transactions) can significantly affect their tax outcomes under the new regime.

Conclusion

In conclusion, the abolition of the non-dom regime and introduction of FIG is a seismic change. It demands proactive planning but also offers opportunities (especially the generous TRF window and the four-year tax holiday for new arrivals). By understanding the rules and acting within the transitional timeframes, advisers can help clients minimize tax impact and comply smoothly with the UK’s new landscape. The UK remains attractive to internationally mobile individuals, but the strategy has shifted from indefinite remittance deferral to maximizing a short upfront exemption period and then integrating fully into the UK tax system. With careful planning one can successfully navigate this transition and make the most of the FIG regime’s benefits while avoiding pitfalls.

Sources:

- HMRC, Residence and FIG Regime Manual – Introduction (RFIG41000) gov.uk

- Saffery Champness, Non-dom tax changes: the FIG regime, CGT and income tax (May 2025) saffery.com

- Saffery Champness, Inheritance tax reforms for UK non-doms (Aug 2025) saffery.com

- Tax Trends, Impact of FIG regime on OWR (Nov 2024) taxtrends.co.uk

- Tax Trends, What is the TRF? (Nov 2024) taxtrends.co.uk

- Low Incomes Tax Reform Group (CIOT), Foreign income and gains from 6 April 2025 litrg.org.uk

- KPMG UK, Mobility Matters – FIG Regime overview (Mar 2025) kpmg.comkpmg.com