Moving from the UK to the UAE: The UK Tax Implications You Cannot Afford to Ignore

The exodus of high-net-worth individuals from the United Kingdom is no longer a trickle. According to Henley & Partners, the UK is forecast to experience a net outflow of 16,500 millionaires in 2025 alone — one of the largest in the world. The UAE, with its zero personal income tax, no capital gains tax, and rapidly maturing financial infrastructure, has become the destination of choice for entrepreneurs, business owners, and wealthy families alike.

But the conversation about UAE relocation is too often dominated by what you gain — and not enough by what you must navigate to leave the UK correctly. This article focuses squarely on the UK side of the equation: income tax, capital gains tax, and most critically, inheritance tax — including the significant and frequently misunderstood risks of establishing a UAE foundation while you are still within the UK's inheritance tax net.

1. Why Clients Are Leaving — The UK Tax Burden

The numbers speak for themselves. A UK-resident business owner extracting dividends from a UK company pays up to 39% tax on those dividends. The same dividends paid to a non-UK resident shareholder in the UAE attract no UAE personal tax at all. That differential alone is enough to transform the financial case for relocation.

Beyond dividends, the accumulation of UK taxes on high earners is punishing:

- Income tax: up to 45% effective rate for high earners

- Capital gains tax: 24% on investment gains and 28% on carried interest

- Inheritance tax: 40% on estates above £325,000 — a threshold that has been frozen for years

The 2026–2030 period is expected to accelerate this trend. Political uncertainty, increased scrutiny of non-domicile status, and ongoing changes to IHT thresholds have combined to make the UAE an increasingly rational choice for international families.

For wider background on the post-2025 changes to the UK tax base for internationally mobile individuals, see our guide to the new Foreign Income and Gains (FIG) regime.

2. Step One: Ceasing UK Tax Residency — The Statutory Residence Test

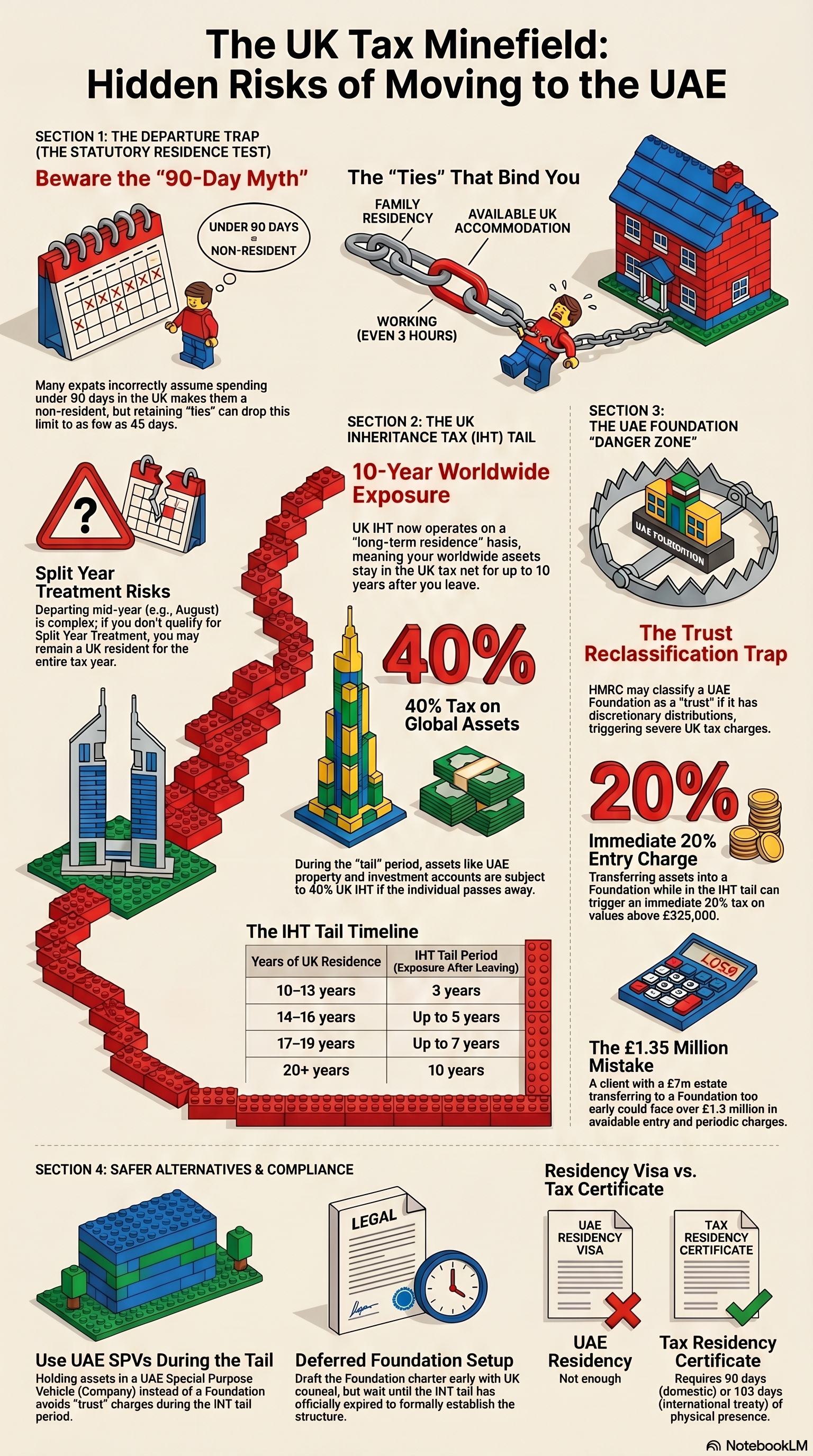

Before any UAE structuring is considered, the most important question is whether — and when — you have actually ceased to be UK tax resident. This is governed by the Statutory Residence Test (SRT), and it is considerably more nuanced than the popular "90-day rule" suggests.

We cover the SRT in more detail in our guide to UK residency rules for leavers and arrivers.

The "90-Day Myth"

Clients routinely tell their advisers that they plan to "spend less than 90 days in the UK" and assume this settles the matter. It does not. Depending on the number of ties you retain to the UK, you may be restricted to as few as 45 days before UK residence status is engaged for the tax year. The SRT operates as a matrix of days and ties — and a single misunderstanding can cost an entire year of non-resident status.

The Key UK Ties

The SRT ties that are most commonly overlooked by clients relocating to the UAE are:

Family tie: A spouse or civil partner, or minor children, who remain UK tax resident while you are abroad.

Accommodation tie: Retaining (or having available to you) a place to stay in the UK — including staying with family members.

Work tie: Performing more than three hours of substantive work on 40 or more days in the UK. A day counts as a working day if you work for three hours or more, regardless of whether you are at a UK office or on a call from a hotel room.

Country tie: Available only to those who have been UK resident in any of the three preceding tax years. It is triggered if you spend more time in the UK than in any other single country in the relevant tax year. This means that even someone spending 80 days in the UAE and 81 days in the UK could satisfy this tie — with potentially serious consequences.

Timing of Departure

Ideally, a client departing the UK should do so on or shortly after 6 April — the start of the UK tax year — to avoid the complexity of Split Year Treatment. If departure occurs mid-year (say, in August), advisers must assess whether Split Year Treatment applies, splitting the year into a UK-resident period and a non-UK-resident period. If Split Year Treatment is not available, the client may be UK resident for income tax and CGT purposes for the entire tax year, even if they physically spent the majority of it abroad.

For mid-year departures, see our detailed guide to UK split-year treatment.

Practical Steps Before Departure

- Obtain a full SRT analysis from a qualified UK tax adviser

- Plan the timing of departure in relation to the UK tax year

- Identify and reduce ties where possible (especially accommodation)

- Create a day-counting and travel log system from day one

- Consider the timing of business disposals or restructurings in relation to residency status

3. Step Two: Capital Gains and Income Tax After Departure

Ceasing UK tax residence removes you from the scope of UK income tax on non-UK source income and capital gains tax on non-UK assets. But several important income and gains obligations persist.

For the wider rules after departure, including UK property, temporary non-residence and remaining UK-source income, see our guide to UK taxation of non-residents.

Rental Income from UK Property

If you retain a UK property and let it out, the rental income remains subject to UK income tax. You must file UK Self-Assessment returns annually to report this income, even as a non-resident. The Non-Resident Landlord Scheme may apply, requiring your letting agent to deduct basic rate tax at source unless you hold an exemption certificate from HMRC.

Employment and Directorship

If you continue to provide services in the UK — including attendance at board meetings — the income attributable to those UK working days is subject to UK income tax. The question of whether management fees or director's fees paid from a UK company to a UAE-resident individual are subject to UK tax depends on where the work is actually performed and whether a double tax treaty applies.

Dividends from UK Companies

One of the most powerful tax planning opportunities available to non-UK residents is the ability to receive dividends from UK companies free of UK income tax. Once you have established genuine non-UK residence, dividends from UK companies are generally not subject to UK withholding tax and are not taxable in the UAE. The timing of dividend extraction — ensuring it falls in a period of non-UK residence but also not in the non-resident part of a split-year — is therefore a critical planning point.

The Departure Return

HMRC operates on a self-assessment basis. Whilst there is no formal obligation to notify HMRC of your departure, it is strongly advisable to file a final UK Self-Assessment return covering the period of UK residence and, where applicable, the non-resident period under Split Year Treatment. This creates a clear record of the date from which non-UK residence was established.

4. Step Three: The UK Inheritance Tax Tail — The Hidden Danger

This is where many clients — and even some advisers — have a significant and potentially costly blind spot.

The common misconception is that once you are physically living outside the UK, your UK inheritance tax exposure ends. It does not. Under reforms that came into force in recent years, UK IHT now operates on the basis of long-term residence rather than domicile alone. The result is a "tail" of continuing UK IHT exposure that can persist for up to ten years after you leave.

We have also covered the new residence-based IHT rules in our 2025 inheritance tax reforms guide and Autumn Budget IHT update.

How the IHT Tail Works

The length of the tail depends on how many years you were UK resident before departure:

| Years of UK Residence | IHT Tail |

|---|---|

| 10–13 years | 3 years |

| 14–16 years | Up to 5 years |

| 17–19 years | Up to 7 years |

| 20+ years | 10 years |

During the tail period, your worldwide assets — not just UK assets — remain within the scope of UK IHT at the standard rate of 40%. The nil-rate band (currently £325,000) still applies, as does the residence nil-rate band where applicable. But for an individual with a £5 million estate, the potential IHT exposure during the tail can be enormous.

What Triggers UK IHT During the Tail

The IHT tail means that:

- If you die during the tail period, your worldwide estate — including your UAE property, investment accounts, and foundation assets — may be subject to UK IHT at 40%.

- If you make gifts during the tail period, those gifts may be potentially exempt transfers or chargeable lifetime transfers, subject to the usual seven-year rule.

- Any structures you create during the tail period may have UK IHT consequences — particularly if those structures are classified as trusts.

5. The Critical Issue: UAE Foundations and the UK IHT Danger Zone

This is the most important section of this article, and the one that catches the largest number of relocating clients off-guard.

UAE foundations — offered through DIFC (Dubai International Financial Centre), ADGM (Abu Dhabi Global Market), and RAK ICC — are highly attractive vehicles for wealth holding, succession planning, and asset protection. They offer:

- Separation of legal ownership from personal ownership

- No UAE inheritance or probate proceedings on foundation assets

- Potential exemption from UAE corporate tax if classified as a family foundation holding long-term investments

- Flexibility through a customisable charter and by-laws

- Alignment with Sharia succession principles where relevant

For a UK person who has fully exited the UK IHT net, a UAE foundation can be an excellent structure. The danger arises when a foundation is established during the IHT tail period.

How HMRC Treats a UAE Foundation

UK law does not recognise a "foundation" as a distinct legal concept. HMRC will therefore look through the structure and classify it according to UK legal principles. The classification will typically be one of three things:

The same structuring should also be checked against the UK’s wider anti-avoidance rules, including TOAA and close company provisions.

1. A trust — if the foundation has characteristics of a fiduciary arrangement (a founder transferring assets to be held for the benefit of beneficiaries, with a governing body acting in a trustee-like capacity). Many UAE foundations, particularly those with discretionary distributions to family member beneficiaries, will be analysed in this way.

2. A company — if the foundation is clearly corporate in nature, with no trust-like features. This is a more favourable outcome from a UK IHT perspective.

3. A bare trust or nominee arrangement — if the founder effectively retains control and enjoyment of the assets, meaning the assets are treated as still forming part of the founder's personal estate.

The IHT Consequences of Trust Classification

If HMRC classifies the foundation as a trust whilst the founder is still in the IHT tail, the consequences are severe:

Entry charge: A chargeable lifetime transfer arises on assets transferred to the trust. This is charged at up to 20% of the value transferred above the nil-rate band (£325,000). For a £5 million transfer, the entry charge could be up to £935,000.

Periodic charges: Every ten years, a "principal charge" arises on the trust's net assets, at a rate of up to 6%. For a £5 million trust, this could represent £300,000 per decade.

Exit charges: When assets leave the trust — whether through distributions to beneficiaries or otherwise — an exit charge arises at up to 6% of the value distributed.

Death during the tail: If the founder dies whilst in the IHT tail period and the foundation has been classified as a trust in which the founder has retained a benefit (a "gift with reservation"), the full value of the foundation assets may be included in the founder's estate for IHT purposes — in addition to any other IHT charges that have arisen.

Consider a client who has been UK resident for 22 years and leaves for the UAE in April 2026. They have a £5 million investment portfolio and a UAE property worth £2 million. They establish a DIFC Foundation six months after arrival, transferring these assets into it.

‣ IHT tail: 10 years (expires April 2036)

‣ HMRC classification risk: The foundation, with discretionary distributions to three adult children, looks like a discretionary trust

‣ Entry charge: Approximately £935,000 (20% × [£7m − £325,000 nil-rate band])

‣ Periodic charge (April 2036): Up to 6% × £7m = £420,000

‣ Result: Avoidable charges of over £1.35 million — simply through poor timing

Had the client waited until April 2036 — when the IHT tail expired — to establish the foundation, no UK IHT charges would have arisen at all.

Drafting Risk: Trust Reclassification

Even where a client is aware of the timing risk and takes steps to structure the foundation as a company rather than a trust, there is a drafting risk. Certain provisions commonly found in foundation charters — particularly around the founder's reserved powers, the discretionary nature of distributions, and the ability to benefit from foundation assets — can cause HMRC to reclassify the structure as a trust regardless of the legal label applied to it.

This is why it is essential that UK tax counsel reviews the foundation charter and by-laws before they are signed, not after.

6. What to Do Instead During the IHT Tail

If you are in the IHT tail and wish to begin asset structuring in the UAE, there are alternatives to a foundation that carry significantly lower UK IHT risk:

UAE Holding Company (SPV)

Establishing a UAE holding company — typically in a free zone such as DIFC, ADGM, or one of Dubai's many free zones — to hold investment assets or UAE property is generally treated by HMRC as a shareholding in a company. This does not give rise to trust charges. The shares in the company form part of your estate in the usual way, but there are no entry, periodic, or exit charges.

UAE Holding Company + Foundation (Deferred)

A practical approach for clients in the tail is to:

- Establish a UAE holding company (SPV) immediately to hold UAE assets

- Draft the proposed foundation structure in advance, with UK counsel sign-off on the charter

- Establish the foundation formally once the IHT tail has expired

This allows the client to benefit from the substance of UAE holding structures from the outset, whilst preserving the option to migrate to a full foundation once the UK IHT risk has passed.

Lifetime Giving During the Tail

Gifts made during the IHT tail period can still be effective for IHT planning — particularly Potentially Exempt Transfers (PETs) to individuals, which become fully exempt if the donor survives seven years from the date of the gift. However, gifts into trust during the tail remain problematic due to the immediate chargeable lifetime transfer charge.

7. UAE Residency and Tax Residency Certificates

One important nuance that frequently surprises clients is the distinction between a UAE residency visa and a UAE tax residency certificate.

Obtaining a UAE residency visa — whether via the Golden Visa, a company visa, or any other route — does not, by itself, make you a UAE tax resident. The UAE Tax Residency Certificate, which is the document needed to claim the benefit of UAE double tax treaties and to evidence UAE tax residence, requires:

- Domestic purposes: Proof of physical presence of at least 90 days in the UAE within the relevant year, plus a UAE bank account and a residential lease

- International treaty purposes: Physical presence of at least 183 days in the UAE within the relevant year

This distinction matters because HMRC will scrutinise residency claims. A client who holds a UAE Golden Visa but has spent only 60 days in the UAE — with frequent travel to the UK, Europe, and elsewhere — may find their UAE tax residency claim challenged.

If a Middle East return disrupts day counts after departure, our note on exceptional circumstances for war-related returns explains when SRT days may be ignored.

8. Compliance Obligations That Persist After Departure

Leaving the UK does not end your compliance relationship with HMRC. The following obligations typically continue:

- UK rental income: Self-Assessment returns must be filed annually to report rental income from UK property

- UK employment or directorship income: Tax returns required where UK-source employment income arises

- UK pension income: UK-source pension income may remain taxable in the UK depending on the applicable double tax treaty (not the case in the UAE however as existing DTA specifically mentions that pension income is to be taxed in the country of "treaty residence" and if that is the UAE therefore taxed at zero).

- Capital gains on UK residential property: Non-residents must report and pay CGT on disposals of UK residential property within 60 days of completion

- Beneficial ownership registers: UK companies and LLPs must maintain accurate PSC (Persons with Significant Control) registers, regardless of the residence of the controller

9. Succession Planning: Wills and Estate Administration

For UK nationals relocating to the UAE with assets in both jurisdictions, a coordinated approach to succession planning is essential.

In the UAE, Sharia law applies as the default in mainland courts. For non-Muslim expatriates, this can produce unexpected results on death — assets may be distributed according to Sharia principles rather than the deceased's wishes. The solution is to register a will through the DIFC Wills Service or the ADGM Wills Service, both of which allow non-Muslims to have their estate distributed in accordance with their own wishes under common law principles.

Clients should also maintain a valid UK will to cover UK-sited assets. A single will attempting to cover both jurisdictions can create complexity and delay in obtaining probate.

The concept of domicile remains relevant even after UK residence has ceased. An individual who retains a UK domicile of origin — without acquiring a domicile of choice elsewhere — may find that certain UK IHT rules apply to their worldwide estate even after the residency-based IHT tail has expired. This is a technically complex area that requires specialist advice.

10. A Practical Checklist: Getting UK Exit Right

Before Departure:

✔ Obtain a full SRT analysis — establish your residency position and identify your ties

✔ Determine the optimal departure date (ideally at or after 6 April)

✔ Quantify your IHT tail exposure (number of UK residence years)

✔ Plan the timing of any asset disposals or business reorganisations

✔ Take UK tax advice on dividend extraction from UK companies post-departure

✔ Draft your final UK Self-Assessment return plan

On Arrival in the UAE:

✔ Obtain UAE residency visa immediately — do not rely on tourist visas

✔ Establish UAE bank accounts and sign a residential lease

✔ Begin accurate record-keeping of UAE presence days

✔ Engage a UAE-licensed CSP (corporate service provider) for structuring advice

✔ Apply for UAE Tax Residency Certificate once qualifying presence is established

Structuring During the IHT Tail:

✔ Use UAE SPVs / holding companies rather than foundations

✔ Draft proposed foundation structure for future implementation

✔ Have UK tax counsel review any foundation documentation before signing

✔ Avoid trust-like provisions in any documentation during the tail period

Post-Tail Structuring:

✔ Establish UAE Foundation (DIFC / ADGM) with UK counsel sign-off on charter

✔ Nest SPVs within the Foundation to hold property, portfolios, and international assets

✔ Execute UAE will (DIFC or ADGM Wills Service) and review UK will

✔ Conduct annual review of compliance obligations in both jurisdictions

Conclusion

Relocating from the UK to the UAE can be one of the most financially significant decisions a high-net-worth individual or family makes. Done well, with proper advance planning, it can legitimately eliminate income tax, capital gains tax, and — over time — inheritance tax on a global estate.

Done poorly, it can leave clients UK tax resident for longer than expected, subject to years of ongoing IHT exposure on their worldwide assets, and facing unexpected IHT charges on UAE structures that were established without regard for the UK rules.

The most dangerous trap is also one of the least publicised: establishing a UAE foundation during the IHT tail period, without UK tax advice on how HMRC will characterise that structure. For a client who has been UK resident for 20 years and transfers a £7 million estate into a foundation six months after departing, the UK IHT entry charge alone could exceed £900,000 — a tax charge that is entirely avoidable with proper sequencing.

The message is simple: plan early, engage both UK and UAE advisers from the outset, and never allow the UAE structuring conversation to happen in isolation from the UK tax position.